Imagine: For several months, you’ve been having pain and stiffness in your hands, especially in the morning. You’ve started taking naps in the afternoon. When you go to your doctor, they take some tests — and you find out you have rheumatoid arthritis. On top of worrying about this new health condition, you also have to think about the cost of treatment. When you search online for the drug your doctor recommends, Stelara, you find out it’ll cost you $850 a month through your Medicare Part D plan.

Getting hit with a high, unexpected prescription cost — especially if you’re living on a fixed income — can be devastating. One way to spread your drug costs out? By enrolling in the Medicare Prescription Payment Plan (MPPP).

The MPPP allows you to fill your prescriptions and pay for them over your plan year. You’ll pay the same amount for the medications, but you won’t have to worry about steep upfront bills. There’s no cost to participate in this program, and all Part D enrollees are eligible. The best time to enroll in the MPPP is at the beginning of the year, but the next best time is today. Keep reading to learn more about how MPPP enrollment works later in the year.

It’s most beneficial to enroll in the MPPP at the beginning of the year, because the amount you pay for medications is spread out over 12 months. This spread is known as prescription drug out-of-pocket maximum smoothing.

But you can opt into the program any time. This is particularly beneficial if you are surprised by an expensive, unexpected drug mid-year. The later you enroll in the year, the more cost compression you’ll have. Your payments will be higher because you have fewer months to pay the bill.

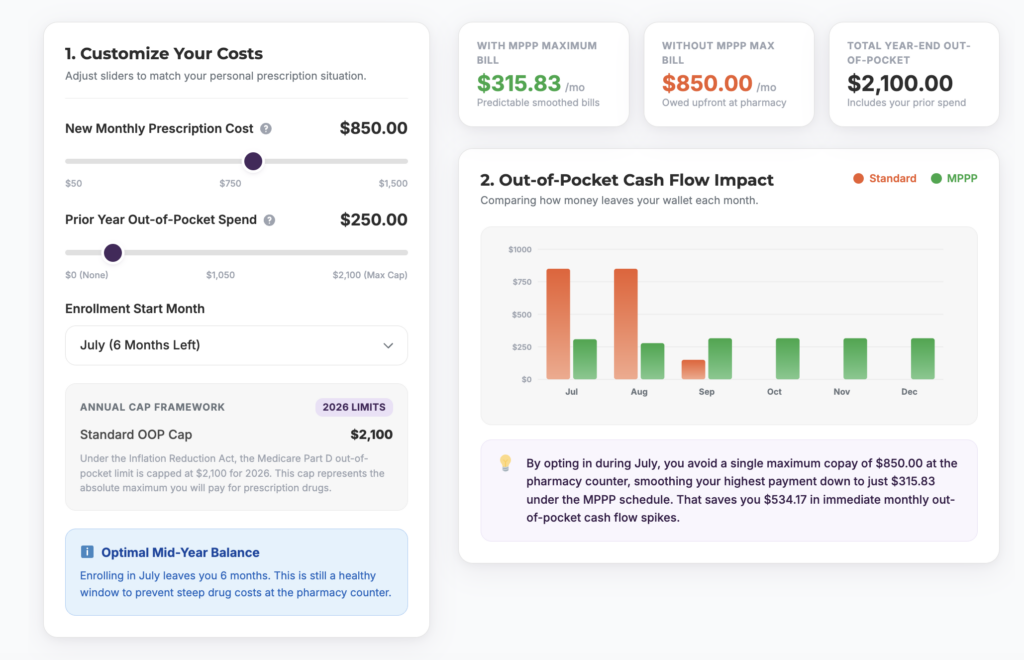

Regardless of when you enroll in the plan, the Medicare Part D prescription payment plan rules are the same. Your monthly bill is based on the cost of your prescriptions, plus your previous month’s balance, divided by the number of months left in the year. Through the program, you will never pay more than the annual out-of-pocket maximum for prescription drugs ($2,100 in 2026).

When you receive your diagnosis of rheumatoid arthritis in July and go to your pharmacist to fill the new $850 prescription, you won’t pay at the pharmacist if you are enrolled in the MPPP. Your new monthly payment is based on what you have already spent on Part D drugs during the year, plus the cost of your drugs for that month. This number is divided by the months left in the year and then billed by your Part D plan.

To see how mid-year enrollment works, let’s look at an example. Imagine you enroll in the program in July after a new diagnosis. You already spent $250 out of pocket on other prescriptions earlier in the year, and your new medication costs $850 per month.

Instead of paying the full $850 at the pharmacy counter in July, your plan caps your first month’s payment using a specific formula: your remaining out-of-pocket limit divided by the months left in the year. The insurance provider calculates your maximum possible payment for that month and always charges you the lesser of the two numbers (the formula cap or the actual cost of the medication).

See below how payments would be set over the rest of the year if you enroll in the Payment Plan in July.

To see how your payments would be calculated for the rest of the year for any monthly prescription costs, visit our Prescription Payment Plan Calculator.

Enrolling in the MPPP is a relatively quick and simple process.

Once your application has been approved, your Part D plan carrier will send you an overview of the program, your enrollment date, and examples of how payments are calculated each month.

It’s important to remember that enrollment into the MPPP doesn’t reduce the total amount you pay for your medication – it just stretches it out over time. To lower your actual costs, you can look into the Medicare Extra Help program (information on this program will be included in your MPPP overview packet). Extra Help is a federal program that assists people who qualify (based on income) with Part D out-of-pocket costs like deductibles and copays. You can be enrolled in both Extra Help and the MPPP.

You’ll get the most benefit from enrolling in the Medicare Prescription Payment Plan if you sign up in January. But MPPP mid-year enrollment can help if you have a large, unexpected drug expense later in the year or find you can’t afford your normal prescriptions all at once. And if your medication costs feel overwhelming, it may be time to consider a new drug plan. Speak with a SmartMatch agent to find the prescription drug coverage that better fits your budget.

Enrollment in a plan may be limited to certain times of the year unless you qualify for a Special Enrollment Period or you are in your Medicare Initial Enrollment Period.

Please log in to view assigned tenants.